by Jason R Owens | Apr 8, 2013 | High Attrition

Your Employees Rule (or at least they should)

A bit of warning before we go any further: on the surface this is going to look like an ordinary get-some-support-staff-for-your-salespeople letter. Resist the urge to go there as I unpack how autonomy is the most powerful force you have in your business.

The answer to getting the most out of your employees is the easiest, yet scariest thing you will ever do — let them decide.

Here’s what a traditional sales role typically looks like:

- Rep is expected to develop relationships with key accounts, identify sales opportunities, and put together deals.

- Also responsible for entering all weekly activities, i.e., meetings, phone calls and all respective notes into company’s customer relationship management (CRM) software.

There is only one problem with this scenario — most sales people can’t stand documentation. It is the bane of their existence. After come cajoling and back-and-forth with leadership, the sales team gets a support person to help with the data entry part of the job.

Here is what the revised roles look like:

- Sales reps – see people and write deals.

- Support personnel – enter meeting notes, track details and handle paperwork.

From here let’s introduce two of the company’s top salespeople – let’s call them Frank and Michelle. Frank fits well into the new system because he hates anything that looks like paperwork. Frank would rather be out on the golf course with a big prospect any day rather than being trapped behind a desk. Frank actually lobbied heavily for the new support person, so, of course, he’s loving the new arrangement. Michelle, is a different story, however.

Michelle came into sales after having spent 5+ years in marketing, so she knows what customers want. Michelle likes the pressure of performing and keeps her own score card. After the sales jobs were redesigned to account for the new support staff, Michelle now feels like she has less time to track her own score. Just last week she decided to take time to do her own numbers, but was caught by one of the members of the sales management team. She was reminded of the investment in the new support person and encouraged to hand off to her score tracker to the new support person. Michelle now gets her scores, but they are at least a week behind, half the data she wants is missing and the report is no longer in a format that she likes. The new system appears to be working well for Frank, but Michelle is quite demotivated because her touchstone — her own version of the score tracker — is gone. Not only is it gone, she is actively dissuaded from doing the work herself. Without this touchstone, Michelle’s work started to slide to a point where she was no longer a top performer.

Let Them Do What They Want

Autonomy is not a one-size-fits-all proposition. This isn’t about designing jobs for a department. It is about designing jobs for individual people. People who bring their own likes, dislikes and preferences to a role. In order for Frank to do his best work he really needs to have a support person handle the details. Michelle needs to have her hands on her score tracker every day. Once Michelle was able to break the ice with her leadership team, she was able to get control of her sales tracker. Less than a month after the change, her numbers started to climb and her performance has fully recovered.

by Jason R Owens | Feb 2, 2013 | High Attrition, New Financial Advisor

New Financial Advisor Success Tactics

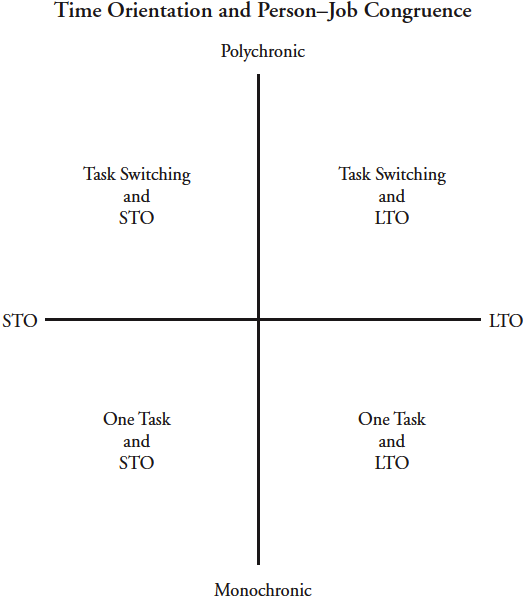

Time Orientation

This is NOT another article on time management. Far from it. Instead, this is an article on preventing stress in your new job.

New Financial Advisors have enough to tend with during their first few months — licensing, class room training, computer-based training, filling the calendar with initial appointments — it can be overwhelming at times. In the midst of this there is one important thing to keep in mind. What is your time orientation?

Researchers Weeks and Fournier (2010) studied how a person’s time orientation contributed to the stress that a person experiences as a sales person. The picture below says a thousand words. There are essentially four major types of time orientation. A person can naturally fall towards a long-term orientation (LTO) or a short-term orientation (STO). Meaning a person’s thoughts and actions fall somewhere on the spectrum between short-term and long-term. There is a second measure that a person needs to consider as well — multitasking. Some people love it. Others can’t stand it. One the graphic you will see the terms polychronic (multitasking) and monochronic (one thing at a time).

Time orientation is important to consider because a sales person who is accustomed to taking a long-term approach to sales will not fit well in an environment that demands short-term focus. The same can be said of task orientation. Some roles demand that the individual focus on many things at once. One could consider a person who does not enjoy multitasking as a poor fit for a job that requires such.

Reference

Weeks, W. A., & Fournier, C. (2010). The impact of time congruity on salesperson’s role stress: A person-job fit approach. Journal Of Personal Selling & Sales Management, 30(1), 73-90.

by Jason R Owens | Nov 14, 2012 | High Attrition

The Secret to Motivating Employees Toward Peak Performance

From time to time we are lucky enough to hire a shooting star, that one employee that is worth 5 or 10 regular players. The holy grail, of course, is getting our regular players to perform like shooting stars. Most of them are quite capable of reaching higher, but year after year they settle for being, well, regular.

The key to employees who are continuously motivated comes from three components:

- Competence – belief that one has the ability to influence important outcomes

- Autonomy – having a choice and fully endorsing what one is doing

- Relatedness – having satisfying and supportive relationships

When all 3 components are at work, employees have higher levels of motivation and put forth more effort.

I am drawing from an impressive body of research from Deci and Ryan who have put their Self-Determination Theory (SDT) to the test in industries as varied as “business, education, sports, medicine, entertainment and leadership” (Stone, Deci & Ryan, p. 76, 2009). The researchers offer the following six practices to creating the environment where continuous motivation will flourish

- Ask open questions and invite participation in problem solving

- Actively listen and acknowledge employee perspectives

- Offer choices within structure including the clarification of responsibilities

- Provide sincere, positive feedback that acknowledges initiative and factual, non- judgmental feedback about problems

- Minimize coercive controls such as rewards and comparisons with others

- Develop talent and share knowledge to enhance competence and autonomy (Stone, Deci & Ryan, p. 80, 2009)

I do not mean to trivialize how important or easy it would be to grow your culture towards continuous motivation, but the rewards are well worth the bumps along the way.

Reference

Stone, D., Deci, E., & Ryan, R. (2009). Beyond talk: Creating autonomous motivation through self-determination theory. Journal of General Management, 34(3), 75–91.

by Jason R Owens | Nov 12, 2012 | High Attrition

Emotional Management for the Small Business Owner

The Path Out of Desperation

Years ago while in the throws of running a business there were times when I absolutely needed a deal. I was desperate. I needed to generate revenue, and the big fish prospect right in front of me had a legitimate need. If I timed this just right I could get myself out of a tight spot. The problem is that the deal never, and I mean never, materialized when I needed it. I was left to scramble to find money elsewhere. I doubted both my calling and my ability. After experiencing this emotional and financial roller coaster enough times I realized that there was only one way out of the doom loop — I had to have more than one big deal in my funnel at a time. I worked extra hard and started putting more and more medium deals in the funnel. These were far easier to get and I started to get good at it. It was a LOT of work, but I managed to do it. I did it so well that I won a sales conference trip that year.

Years ago while in the throws of running a business there were times when I absolutely needed a deal. I was desperate. I needed to generate revenue, and the big fish prospect right in front of me had a legitimate need. If I timed this just right I could get myself out of a tight spot. The problem is that the deal never, and I mean never, materialized when I needed it. I was left to scramble to find money elsewhere. I doubted both my calling and my ability. After experiencing this emotional and financial roller coaster enough times I realized that there was only one way out of the doom loop — I had to have more than one big deal in my funnel at a time. I worked extra hard and started putting more and more medium deals in the funnel. These were far easier to get and I started to get good at it. It was a LOT of work, but I managed to do it. I did it so well that I won a sales conference trip that year.

The Secret of Inventory

One of the tools that I found invaluable is a simple low-tech tool called a follow-up file. This is NOT your to-do list for closing a deal. Instead think of this a long-term follow-up. This is where you capture every last time a client says “I’m not interested now, but after (insert reason here) the vacation is over, school starts, the beginning of the year, etc. I would write it down. Every one of them. Try this yourself. If you are in a business where you talk to new prospects 5-10 times per week, you will amass a good inventory in about 90 days. The great part about this that once you get into the rhythm of entering items into your follow up file, you won’t want to stop. My big surprise was looking back on this list from a harvest perspective after 3 months. I had managed to stack up several pieces of low hanging fruit. Many of those “call me later” deals were ripe for the picking. It worked great.

What Exactly is a Sales Funnel?

In this case a picture is worth a thousand words. For the uninitiated a sales funnel is simply a list of all your deals, and the list is segmented by stages. Some deals are just at the beginning stage while others are just about to be closed. When you get up each day, take a look at your funnel and ask one important question – “What do I need to do today to move each of these deals to the next step in the funnel?”

In this case a picture is worth a thousand words. For the uninitiated a sales funnel is simply a list of all your deals, and the list is segmented by stages. Some deals are just at the beginning stage while others are just about to be closed. When you get up each day, take a look at your funnel and ask one important question – “What do I need to do today to move each of these deals to the next step in the funnel?”

What do I need to do today to move each of these deals to the next step in the funnel?

It is a simple question that cuts through all the clutter and distraction. If today’s to-do list does not include directly moving all of your deals an inch closer to your wallet, you are working on the wrong things.

Take Aways

Here is a list of the top things you can do to keep your head in the game.

- Commit to building an inventory. No technology required. Just use a yellow pad of paper or a white board in your office. Write down every deal that you see, no matter how far out in the future it may be. Revisit this list often. You’ll be glad you started.

- Track all your prospects in a sales funnel. Make it your mission everyday to move each deal one step closer to completion.

- Work hard. Yes, that’s right. Work hard. Your dreams are in reach.

by Jason R Owens | Aug 10, 2012 | High Attrition, New Financial Advisor

For Some New Financial Advisors, Solo is the Way to Go

For Some New Financial Advisors, Solo is the Way to Go

New financial advisors face enough hurdles in their first 24 months — licensing requirements, developing new skills, information overload. It can be a lot to absorb. The last thing you want to do is complicate things by trying to take on too much, especially if you lose focus on obtaining new clients.

In my time as an advisor an a coach to advisors I have only seen a handful of advisors who are able to make a solo practice really work. Most have far too much unpaid work on their desks, or their lives are ruled by incoming service calls. Unless you are paid specifically for doing service work, you will want to steer clear of being completely on your own, even in the first 24 months.

Pros

Low overhead

The good part about being solo is the low overhead. You can work from your home or in a respectable key man office space. Since you are doing all the work you have no staff to pay.

No workflow issues

Again, since you are working by yourself you do not need to be so concerned with not knowing what is happening in your office.

No office politics

I know of many wage earners who love their jobs, but would trade-in their co-workers in a heartbeat.

Cons

Details

It is pretty common to need to juggle reworking your calendar to fit in Mrs. Jones who wants to rearrange her appointment with you for afternoon on Friday even though you have a standing policy against taking clients on Friday afternoon; working on an analysis but getting interrupted by a service call at a critical point; writing a note about a client’s low priority issue that you plan on handling tomorrow after your analysis is done; placing a 48 minute phone call to tech support because your printer will not print the analysis you just finished; and looking for the handwritten note that you lost regarding the customer (can’t remember her name now) who called yesterday wanting her dividend option changed. All this can happen over the course of only a few hours. It can be a lot to remember. If you are good with details, you will get your chance to push your limits in this new role.

Alone

Some people simply enjoy a little camaraderie once in a while, so being on their own is quite easy for them. Others simply have a hard time working alone all day. These people crave interaction, and one more webcam meeting isn’t going to suffice. It has to be a live person-to-person meeting for it to count.

by Jason R Owens | Aug 9, 2012 | High Attrition, New Financial Advisor

Is New Financial Advisor Failure Preventable?

Perhaps if we study why a new financial advisor tends to fail at such an alarming rate we’ll be able to find ways to prevent it. In this blog post I have captured a few articles that grabbed my attention lately. You should find a broad scope of articles here for people who are captive agents, independent agents and from the world of online insurance sales.

While Why I Failed as a Broker is a little dated (2006) many aspects of the article still ring true for today’s new financial advisor. For example, the author of this article said that he was attracted to the business because he wanted the chance to manage money. Later in his stay he realized that he could only afford to spend about 5% of his time on actual money management because he needed the other 95% of his time to prospect for new business. Another interesting point about the article is that the author is not complaining — he does not blame his company. Click through to the article to learn more.

Why Agents Fail talks about the importance of new financial advisors having good communication skills, staying up to date with your product offering and keeping pace with new technology. It is written by a company that does online insurance sales.

The Top 7 Reasons New Insurance Agents Fail to Reach Success offers some good insight for those who are able to take advantage of an independent insurance agent platform. For those of you who happen to be on an independent platform, this article is quite good. New financial advisors who are captive agents may face a few restrictions in implementing the approaches listed here.

Why 77% of Insurance Agents Fail Within the First 6 Months appears to be a sponsored article written by a company that sells a marketing system. The four primary steps of their system are Interrupt, Engage, Educate and Offer. What I like most about this article is the all-too-real depiction that the author gives of what a new advisor faces in his or her first few years.

Why do 95 percent of Insurance Agents Ultimately Fail? is written by Lew Nason out of Dallas, GA. Lew’s stance in this article is that hiring a mentor is a really good idea, and he gives you some advice on how to properly hire a mentor that will provide you with a positive return on your investment.

Here are two others that caught my eye while researching.

In Are Financial Advisers Failing the 99% the author makes the case that the average american just isn’t being served well by the typical financial advisor. The reason: advisors just don’t make a great deal of money on people who have less than $100K of investable assets.

In Financial Advisors Flunk the Undercover Sting we find role playing taken to a new level. Only the advisors didn’t know they were role playing. Researchers from MIT and Harvard hired actors to play affluent couples and sent these prospects to visit firms in the Boston area.

by Jason R Owens | Aug 7, 2012 | High Attrition, New Financial Advisor

Two Ways New Financial Advisors Can Cope with Failure (second in a 2 part series)

In my previous post on What to do with Failure?, I mentioned that new financial advisors tend either to internalize their failures (it is always my fault) or to externalize their failures (it is always the prospect’s fault). How do we resist the urge to feel overwhelmed (with a sense of self-loathing) or misunderstood (All these people just can’t get it right)? Those who tend toward internalizing will need to travel by one road, and those who blame others will need to travel by a different road.

For New Financial Advisors who Internalize

There is no going around this mountain. There are tough lessons here to be learned, and the only way past this mountain is to go through it traveling the path of pain. You will most likely experience adversity when trying to set appointments. For some, you will be fortunate enough to be assigned some orphan clients who have a relationship with the company. For others you will need to build rapport through calling a list or by phoning friends and family. To many this will seem like an exercise in torture at first. But, it gets easier. Once you find this not so painful you will move on to the next step. People who stand you up for appointments.

You may travel to their house to find that the prospects are not there, or you will find that the prospect insists on a 7:30 PM meeting at the office and then fails to show. Again, you endure this a few times and you find that it isn’t the end of the world. You graduate to setbacks dealt to you by Compliance or by Underwriting or by predecessor companies who do not transfer money quickly enough, etc. The point here is that you probably need to experience losses in each of these areas a few times before you are able to shrug it off as being not such a big deal. The problem that new financial advisors face is getting surprised by these setbacks when they least expect it.

For New Financial Advisors who Externalize

The number one work that I can offer here is ownership. Chances are pretty good that everyone else is not the problem. You screw up, too. Own it. The only way for you to get the benefit from your experience is to admit that you had some part in this two-person dance’s not working. Once you are able to reach this hurdle, you can then see more clearly what steps you could have taken to save the deal.

Final Words

In this article I provided more depth on what new financial advisors can do to recover from failure. In my next article I will introduce a third response – making note of what happened, and then moving on. Remember that resilience is one muscle that can not be built without use. No one can do this for you, and you can’t get better at it by reading a book or watching a video. Resilience is best developed through hardship.

by Jason R Owens | Aug 7, 2012 | High Attrition, New Financial Advisor

Two Ways New Financial Advisors Can Cope with Failure (first in a 2 part series)

In my past few posts to new financial advisors I wrote that you should not blame yourself if you find this business is not all that you had expected. I also wrote a piece on getting your emotional game in line before you attempt the numbers game. I feel that I can’t do this latter issue enough justice, so I’m writing on it again today.

Your emotions come from the heart. Why does a failed case send you into a tailspin? When a client who loved you last week does not return your calls this week, why do you freak out about not having enough money in the pipeline? If you are running behind on your production schedule, why do you lose sleep over it? These fears strike at the very core of our identity sometimes. When a deal that was “in the bag” suddenly dries up, you could interpret that as your not being good enough to save the deal. That somehow it is a shortcoming on your part. You may have internalized the failure. Or, you could blame the prospect for being a flake. After all, you did your part of the bargain.

I have seen many new financial advisors internalize failure. I tend to do this myself. Somehow I should have been smart enough, good enough, fast enough or fill-in-the-blank enough to get the prospect to close the deal. It is great to learn from failure, but there’s a danger in blaming yourself as you could become paralyzed with self-doubt or feelings of inadequacy. If you give these feelings time to take root, your business is doomed.

On the other end of the spectrum are the new financial advisors who externalize failure — it is someone else’s fault. While these individuals typically do not learn much from failure, they are not paralyzed by it either. In their minds the prospect is always the one causing the problem — the prospect got cold feet, the prospect didn’t turn in the paperwork, the prospect got too busy to return calls. Again, externalizing can be a healthy way to respond to a setback in your sales efforts, but I have also seen this mindset bleed over to interpersonal dynamics with fellow team members (The other guy is the problem; there is nothing wrong with me), but I’ll save this item for a post at a later time.

The most important thing that you can do with failure is to learn from it but not dwell on it (much easier said than done for those analytical-thinker types out there). Failure must be framed in your head as something that polishes you, not something that drains you. It adds to your repertoire for the next prospect meeting. This is the school of transactions. You learn by doing. Managing your emotions is a choice that we make day by day and hour by hour. The better you get at this skill, the better you’ll become in all aspects of your life.

by Jason R Owens | Jul 29, 2012 | High Attrition, New Financial Advisor

As a new financial advisor (new FA) sometimes you just find yourself in a bad situation. After weeks and weeks of licensing efforts maybe you are behind in production, or perhaps the portion of your income that is steady is about to run out. You might be frustrated and wondering how you worked yourself into this position. You have to remind yourself one simple thing…

As a new financial advisor (new FA) sometimes you just find yourself in a bad situation. After weeks and weeks of licensing efforts maybe you are behind in production, or perhaps the portion of your income that is steady is about to run out. You might be frustrated and wondering how you worked yourself into this position. You have to remind yourself one simple thing…

It’s not your fault.

There is a very well oiled machine that brought you to this point. The machine is doing its job — it is recruiting qualified people into an organization. You can take some comfort knowing that dozens or hundreds of other people in your recruiting class had to pass the same entrance qualifications that you did. For every person who made it to where you are know, 22 others didn’t make the cut. Maybe they didn’t pass the original assessment that you passed. Maybe they didn’t pass the interview that you passed. Maybe they didn’t pass all the licensing exams that you passed. You made it. They didn’t.

Even though you survived the cut you may be thinking that you wish you hadn’t. You may not have fully understood what you were signing up for. Sure, you were probably told at some point that you were going to have to reach a production hurdle, but how do you gauge that when you’ve never been in production before? If you were given a number, did you fully understand what that meant for you? Did you really know what assets under management (AUM), production credits, or accumulated base commission (ABC) meant for you as far was your workload was concerned? If you answered “no” to this question, don’t despair. Most people don’t really know what they are signing up for when they say “yes” to this job.

by Jason R Owens | Jul 24, 2012 | High Attrition

Again we turn our attention to one of the hottest growing insurance markets in the world for a few lessons. The insurance market in China has until recently been concentrated in metropolitan areas. Given China’s rising middle class insurance sales has spread to rural areas. It is reported that China has 83,000 representatives in the Sichuan provence alone (Tian, 2011). Tian (2011) performed a study that suggested rural insurance salespeople thrive on training.

Those with more training have significantly higher sales in terms of First Year Premium.

Agents reported a preference to group meetings rather than self-paced training. As a bit of commentary I will add that it is interesting to see where the Chinese insurance market is in relation to training. It appears that the US companies are continuing the ever-present push to reduce training amount and training dollars. It may be that the Chinese insurance market is in such a period of growth that it is easier to spend money on training. As this new market matures over the next 20-30 years it will be of interest to see if spending on training tapers off as growth slows.

Reference

Tian, W. (2011). Study on influencing factors of rural insurance salesman’s sale performance. International Journal of Business and Management. doi:10.5539/ijbm.v6n5pl80

{kind=link}